The United States has entered a period of systemic failure where the digital ambitions of the artificial intelligence revolution are being throttled by the physical limitations of 20th-century industrial infrastructure. As of April 2026, the strategic mismatch between software innovation and grid capacity has moved from a supply chain nuisance to a full-scale national security crisis. This report evaluates the bottlenecks—from local regulatory friction in Northern Virginia to a “Physical Layer Embargo” driven by global manufacturing disparities—that currently threaten American technological primacy and AI sovereignty.

The Northern Virginia Flashpoint: The Digital Gateway and Project Attrition

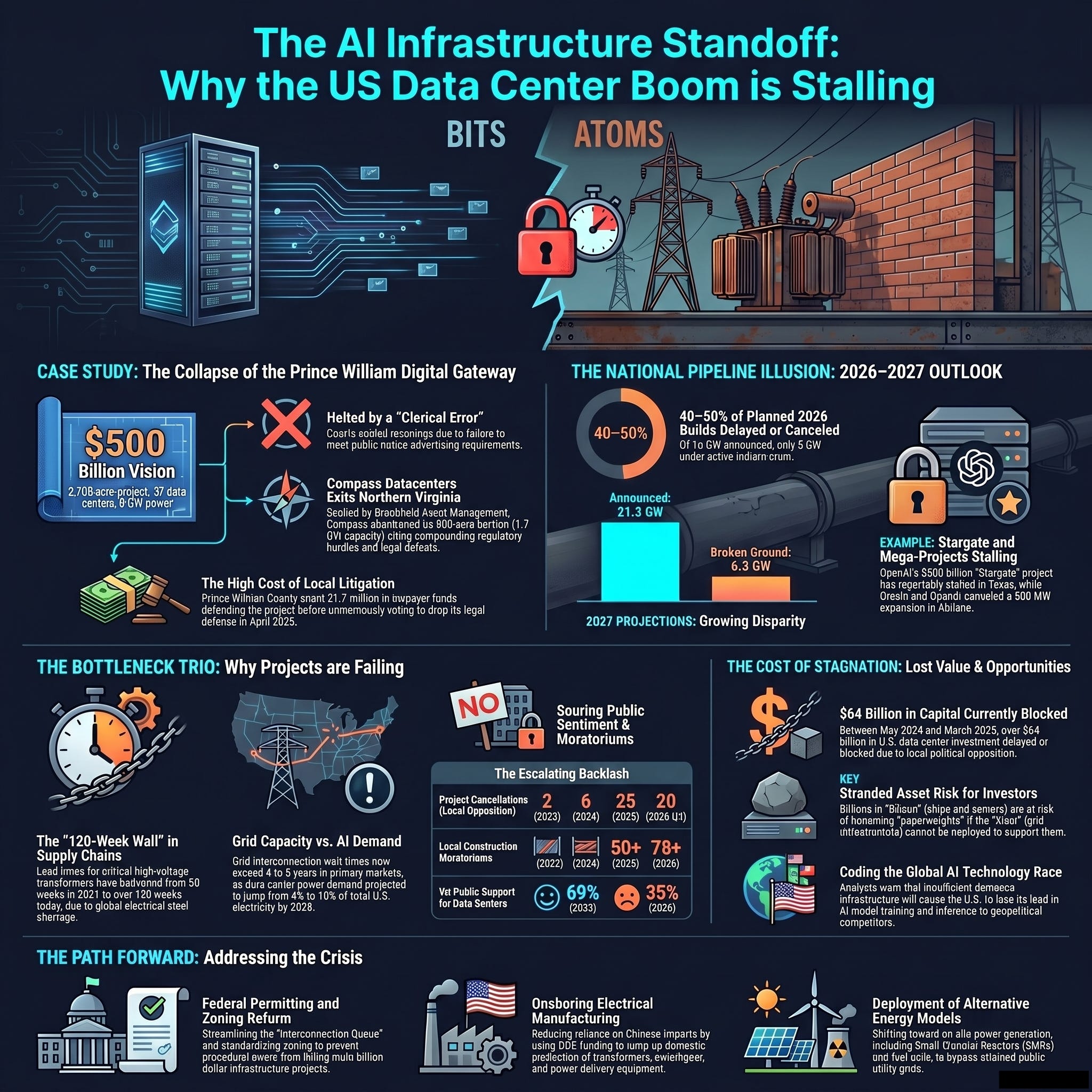

Northern Virginia, the global epicenter of data center density, has transitioned from a growth engine to a strategic warning zone. The shelving of the “Project near Manassas” (Compass context) is a harbinger of a broader trend: the collapse of megaprojects under the weight of regulatory and civic friction. The PW Digital Gateway, a 2,139-acre corridor once envisioned as a world-class technology hub, now serves as the primary case study for “Project Attrition.”

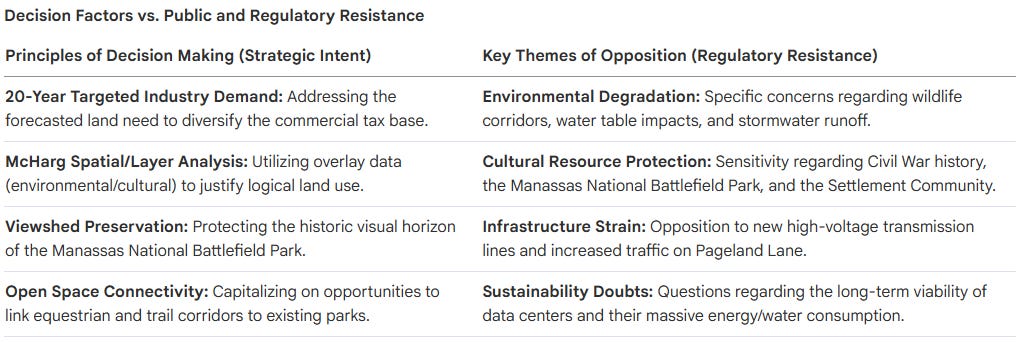

Based on the PW Digital Gateway Staff Report, the friction originates from a fundamental conflict between targeted economic expansion and non-negotiable cultural preservation. Policy advisors must recognize that traditional data center architecture is no longer viable in high-sensitivity corridors where “Viewshed Analysis” dictates site feasibility.

In this regional conflict, environmental and historical protections for the Manassas National Battlefield Park and the Conway Robinson State Forest have become non-negotiable blockers. Current mandates now enforce strict height limitations by district: building heights are capped at 45 feet in the Southern District (to preserve Battlefield/Forest proximity) and 85 feet in the Northern District. Furthermore, facades must utilize non-reflective earth tones to blend into the tree line. These constraints, combined with local litigation, have transformed the “path of least resistance” into a landscape of stranded capital.

A Landscape of Scrapped Megaprojects: The Scuttled U.S. Pipeline

Data centers, once the sole bright spot in the U.S. construction market, are now experiencing a catastrophic downturn. Project cancellations have quadrupled, jumping from six in 2024 to 25 in early 2025. This is not a series of isolated local disputes; it represents a systemic failure of the National Interest to align local land use with federal technological goals.

A primary casualty of this crisis was the AWS Oregon Data Center Cluster (75 MW). Originally designed to utilize on-site natural gas-fed solid oxide fuel cells (SOFCs), the project was scrapped in June 2024 due to regulatory hurdles. The strategic lesson is stark: the industry’s heavy reliance on self-operated, fossil-fuel-dependent models is increasingly untenable. The pivot from direct operation to utility-backed “behind-the-meter” partnerships is now a survival requirement.

Regulatory High-Water Marks

Legislative and grassroots blockers have established a new ceiling for hyperscale growth:

Maine Moratorium Bill: Legislative action targeting projects over 20 MW, effectively freezing development until late 2027.

The Hilliard Opposition (Ohio): Grassroots challenges and legal battles over “behind-the-meter” power plants, specifically targeting industrial-scale natural gas pipelines and diesel generators.

Virginia Legislative Shifts: A wave of state-level proposals for construction bans and increased oversight in formerly “pro-data center” jurisdictions.

The “120-Week Wall”: Quantifying Financial Loss and Stranded Asset Risk

The U.S. is currently hitting the “Silicon vs. Steel” wall. While software development follows a 24-month refresh cycle, physical grid infrastructure operates on a mid-20th-century industrial timeline. This 10x latency gap between “bits and atoms” has created a structural bottleneck that capital alone cannot resolve.

The $483 Billion Execution Gap

The financial implications of this mismatch are devastating. Big Tech is projected to spend 650–700billion∗∗onAIinfrastructurein2026.However,ofthe16GWofplannedcapacity,only5GWiscurrentlyunderconstruction.This∗∗69483 billion in capital is effectively chasing non-existent steel.

This bottleneck is rooted in non-negotiable physical constraints: the global scarcity of Grain-Oriented Electrical Steel (GOES) and the specialized 50-year curing cycles required for transformer oil. Money cannot manifest specialized foundries or accelerate chemical curing overnight. Without these components, multi-billion-dollar GPU clusters remain stranded assets.

The AI Technology Race: Geopolitical Risks and Lost Opportunities

The infrastructure crisis has evolved into a direct threat to AI Sovereignty. The inability to energize data centers at the speed of software development has handed a strategic advantage to global rivals.

Geopolitical “Physical Layer Embargo”

The disparity between U.S. and Chinese manufacturing capabilities represents a critical strategic disadvantage. China currently dominates roughly 60% of global transformer production capacity.

The Lead Time Disparity: Chinese manufacturers can produce transformers in 48 weeks, while U.S. lead times have ballooned to 143 weeks.

Refresh Latency: China can refresh its physical AI infrastructure three times in the same period it takes the U.S. to energize a single site.

Import Dependency: Through October 2025, the U.S. was forced to import over 8,000 high-power transformers from China—a 533% increase from 2022 levels.

The Cloud Capacity Crunch

This physical shortage has triggered a downstream “Cloud Capacity Crunch” for U.S. developers:

GPU “Sold Out” Status: Hyperscalers have locked in NVIDIA Blackwell GPUs through 2027 but lack the energized data center shells to house them.

Pricing Spikes: On-demand compute pricing has surged 2–3x higher than reserved capacity, pricing out American startups and hobbyists.

Competitive Attrition: While U.S. developers face a 3–5 year wait for hyperscale capacity, global rivals with faster physical infrastructure deployment are capturing the market for high-density training runs.

Strategic Remediation: Accelerating the Path to Energization

To ensure AI resilience, infrastructure planners must pivot from “Grid-Dependent” models to Strategic On-Site Power.

The “Ohio Model” and the Authority Conflict

The partnership between AEP Ohio and AWS (72.9 MW of SOFCs) serves as a replicable template for “Behind-the-Meter” generation. By directly funding infrastructure, AWS bypasses the 3–5 year transformer queue. However, this model is currently threatened by the Hilliard Lawsuit, a “State vs. Local” authority conflict where municipalities are challenging the state’s power to permit “mini gas power plants” in residential proximities. Solving this jurisdictional friction is a prerequisite for national scaling.

Multi-Track Solution List

Near-Term (The 90-Day Antidote):

Modular Power Systems: Utilizing Siemens/Eaton systems to cut two years off deployment.

Natural Gas SOFCs: Deploying Bloom Energy fuel cells, which offer a 90-day deployment window compared to the 3–5 year grid wait.

Mid-Term:

Edge Computing: Shifting workloads to distributed infrastructure with 6–18 month timelines.

Hydrogen-Fed Fuel Cells: Transitioning to green hydrogen to mitigate local environmental opposition.

Long-Term:

Small Modular Reactors (SMRs): Direct investment in “behind-the-meter” nuclear power for 2028–2030 deployment.

A Strategic Imperative

Infrastructure planners must treat transformer lead times and GOES scarcity as the critical path for all technological development. The U.S. cannot win the AI race with 21st-century software and 20th-century steel. We must adopt a pragmatic, dual-track approach: deploying natural gas SOFCs as an immediate bridge while aggressively building the domestic manufacturing base for the green hydrogen and nuclear foundations of the future. Failure to align physical infrastructure with digital ambition is no longer an option—it is a surrender of AI Sovereignty.